FBT Changes in the 2026 Budget

A More Practical Road Ahead?

The FBT proposals tabled in 2025 led to significant backlash against what many called “Ute Tax 2.0”. The updated proposals included in Budget 2026 appear to be a genuine attempt to meet those concerns, while also simplifying the FBT motor vehicle rules.

The changes also recognise that vehicles, work patterns and technology have moved on significantly since the FBT rules were first introduced in 1985.

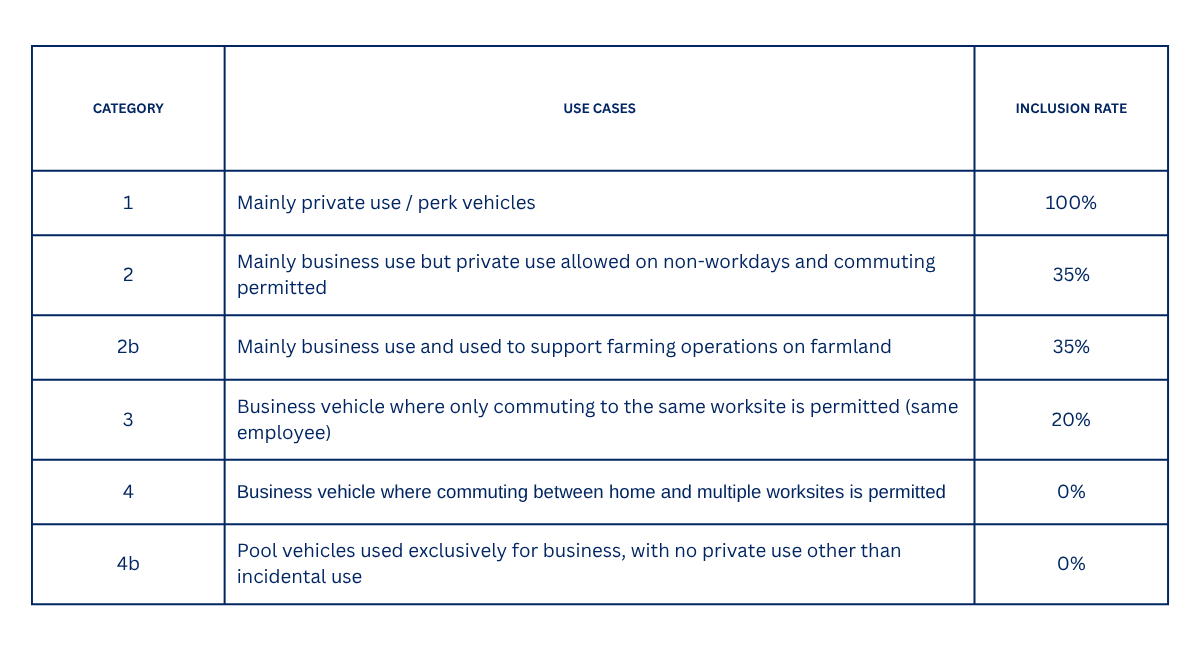

The key proposal is to replace the current day-counting approach with a category-based regime from 1 April 2027. Instead of tracking the exact number of days a vehicle is available for private use, employers would classify each vehicle based on its expected use and apply a set “inclusion rate” when calculating FBT.

The proposed categories are:

The Work-Related Vehicle Exemption Is Going - But Not Really

The work-related vehicle exemption is still going. However, the new Category 2 treatment is designed to produce a similar outcome for many work vehicles that are currently treated as exempt during the working week, but subject to FBT on weekends, public holidays, annual leave days or rostered days off.

The new 35% category is specifically designed to reflect this common usage pattern. Inland Revenue’s own example makes this clear. A branded ute used for work during the week, with private use allowed on weekends and public holidays, would fall into Category 2 and be subject to FBT at a 35% inclusion rate. Inland Revenue compares this with the current rules, where FBT would often be paid on Fridays, Saturdays and Sundays, equating to roughly 40% of the quarter.

A Shift Away From Utes

One of the more welcome aspects of the reforms is that concessionary treatment is no longer tied to a particular type of vehicle. This should reduce any distortion created by the current rules, where businesses may have chosen utes for tax reasons rather than operational need.

The revised approach focuses more on how the vehicle is actually used. Branding, business use, value, restrictions on private use, and whether the vehicle is shared will all be relevant. A “normal car” may qualify for lower FBT rates if it is genuinely used for business purposes.

Better Treatment for Hybrids and Electric Vehicles

The current FBT rules have often produced odd outcomes for businesses seeking to transition to lower-emission fleets.

A hybrid or electric car or SUV used predominantly for business purposes generally could not access the same concessions available to a sign-written ute being used in a very similar manner. This created a tax disadvantage for businesses attempting to move toward lower-emission vehicles.

The Budget proposals address this issue in two ways.

- First, concessionary treatment is no longer restricted to particular vehicle types.

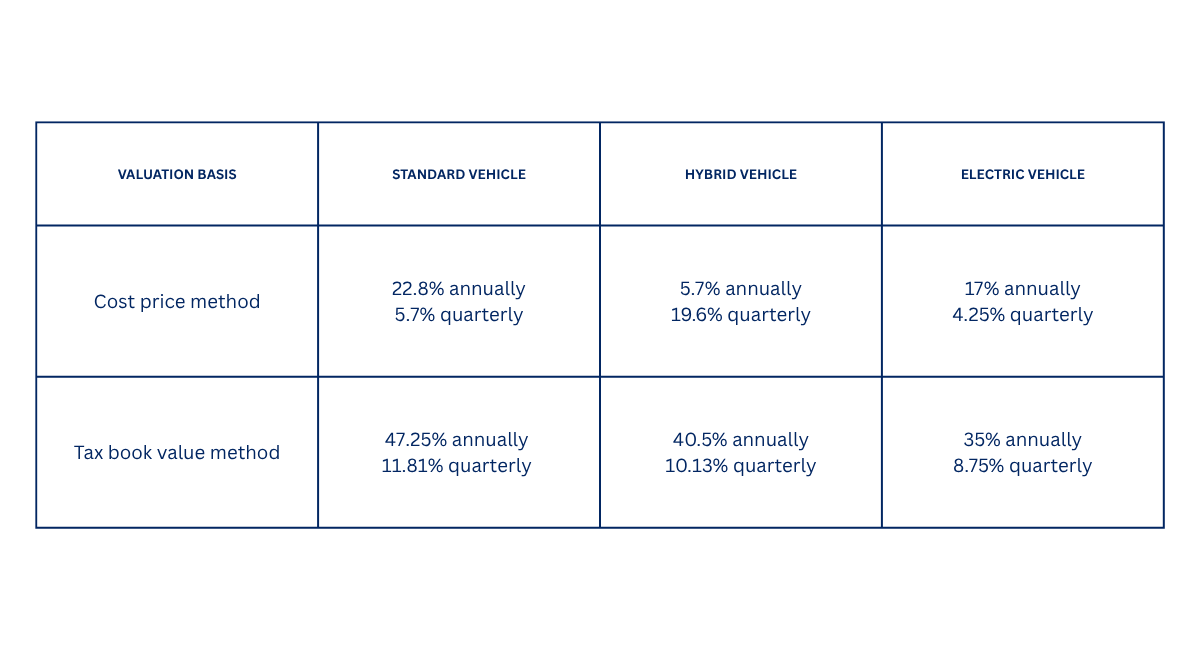

- Second, the proposals introduce different valuation rates depending on fuel type:

These rates include a 12.5% discount to reflect periods where the vehicle may not be available for private use, for example due to mechanical issues. The tax book value rates also assume Investment Boost has been claimed.

The new rates are higher than the current standard rates for ICE vehicles, but discounted rates apply for hybrids and EVs to reflect lower operating costs.

Our thoughts

There will still be opposition to the removal of the work-related vehicle exemption. However, much of that opposition is likely driven by the misunderstanding that work-related vehicles were fully exempt from FBT. They were not.

The current regime requires careful monitoring of vehicle availability, restrictions on private use, exempt days and logbooks. In practice, that has made compliance difficult and inconsistent.

The options were either for Inland Revenue to enforce the current rules more strictly (and a sign-written ute towing a boat was always going to be easy to spot) or to modernise the regime so it better reflects how vehicles are actually used.

The updated proposals appear to strike a more sensible balance.

Businesses should start reviewing their vehicle fleets now. In particular, employers will need to consider which category each vehicle is likely to fall into, whether branding is required, what private use restrictions are in place, and whether employment agreements and vehicle policies align with the new rules.

Disclaimer

The information provided in this article is general in nature and does not constitute personalised tax advice. The proposed FBT reforms are subject to legislation and may change before implementation. You should seek professional advice tailored to your specific circumstances before making any business or tax decisions based on this content.